Bad credit. It doesn’t have a fine ring to it, but it’s an important topic to highlight. Obtaining a home loan has become more difficult as the banks alter their lending criteria. Becoming aware of having bad credit is more important than ever.

Bad credit history can linger for many years, restricting you from lending the right loan or possibly any loan for that matter. So, here’s what you need to know about improving your credit rating.

Your credit file contains lots of lending activity. If you’ve applied for a loan, defaulted on loan repayments or entered into a debt agreement, all these entries are recorded and will remain on file for several years.

What is bad credit?

Bad credit is bad news… It includes information relating to missed repayments, debt agreements (which are also known as payment plans), loan defaults and even bankruptcy. This information is then assessed and calculated to determine your credit score. Ultimately resulting in good credit or bad credit.

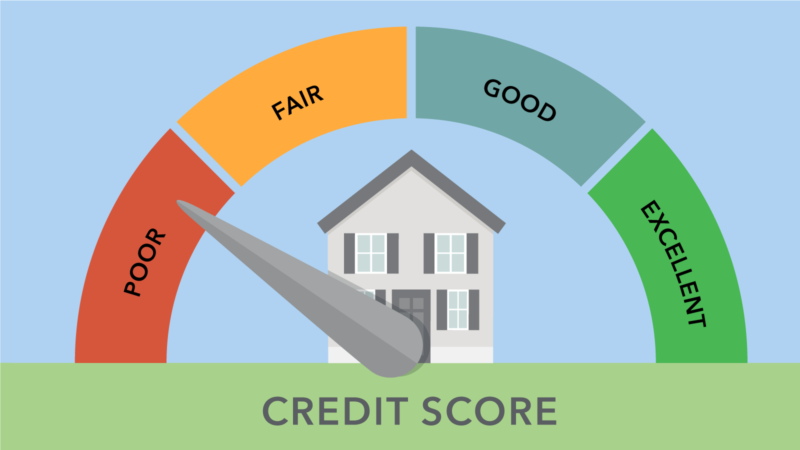

The scoring is placed in categories from excellent-very good-good-fair-weak. These scores will greatly affect the lender’s appetite to borrow your money. It allows them to identify the risks associated with entering a loan agreement. If you have any bad credit recorded on file, this will immediately highlight a concern for the lender. It is a high trigger of being rejected for finance.

Due to the importance of finance, we highly recommend seeking advice from a mortgage broker. To further understand the importance of hiring a mortgage broker, please refer to our article of “The mortgage broker – Why we recommend using them“.

Can we still get a loan with bad credit?

There are many specialised financiers that offer loans to borrowers retaining average or bad credit. Unfortunately, many borrowers in this situation may then be persuaded to accept finance by a lender that incurs higher interest rates and fees. The increased costs may cause large problems by default and/or bankruptcy.

Do your research and review your cash flow. Ensure you are in a position to service the increased costs and further evaluate if the decision to buy a property is worth the extra cost.

How long does bad credit remain on file?

The types of credit issues remain on your file differently. In short, bankruptcy is listed on your credit report for up to five years from the date you declare it. This can last longer depending on the outcome and severity. Other databases can keep this on file indefinitely. Entering into a debt agreement will last for five years, or potentially longer in some circumstances. Incurring a credit default will remain on your report for five to seven years.

There are many other types of bad credit implications, however we have named the more common and well-known events.

What can I do to improve my credit?

There are many strategies that can be adopted to improve your credit score. We recommend consulting your financial adviser and mortgage broker. There are many specialists that can tailor a plan to advance your situation sooner.

How do I know when I can buy a property?

Firstly, and utmost importantly do not enter a contract of sale prior to understanding your credit rating. You can obtain a copy of your credit report from multiple companies. Don’t allow impulse buying to distract you away from understanding your borrowing capacity.

Take some time to consult a mortgage broker in advance to buying. They can also help you become more aware of your credit rating and help you understand if you are in the right situation to borrowing funds to invest.

If you want to learn more about bad credit, please contact us. We can introduce you to a qualified person.

While we have taken care to ensure the information above is true and correct at the time of publication, changes in circumstances and legislation after the displayed date may impact the accuracy of this article. If you want to learn more, please contact us. We welcome the opportunity to assist you.

August 2018

Clyde North – Northside estate

Clyde North, Melbourne, City of Casey, Victoria, 3978, Australia Details

Deanside – NDIS Property

Deanside, Melbourne, City of Melton, Victoria, 3336, Australia Details

Bonnie Brook – Oaklands estate

Bonnie Brook, Melbourne, City of Melton, Victoria, 3335, Australia Details

Surrey Hills – Surely spectacular

Surrey Hills, Melbourne, City of Boroondara, Victoria, 3127, Australia Details

Geelong – NDIS Property

Geelong, City of Greater Geelong, Victoria, 3218, Australia Details

Sunbury – Everley estate

Sunbury, Melbourne, City of Hume, Victoria, 3429, Australia Details

Sunbury – NDIS Property

Sunbury, Melbourne, City of Hume, Victoria, 3429, Australia Details